I thought I would write about something that we are starting to see more and more of and it really bothers me. Banks offering insurance. I have a friend in the home and auto insurance business and he told me about a story involving a client and a Calgary car dealership. The dealership had sold the client a new truck and along with it some type of loan protection policy. They don’t really call it life insurance, but the idea being that if the client dies, the bank (underwritten by an insurance company) would pay out the loan, so that the beneficiary of the truck doesn’t have to take on the burden of paying off the truck.

Here’s the problem with an offer like this. The truck was $90,000 to buy and the term of the loan offered by the dealership was for 7 years. The client was quoted $7,000 over the 7 years. Apparently, the dealership didn’t explain to the client that she didn’t need the coverage. In fact they suggested that in order to get the loan secured she would have to get the coverage.

To put this in perspective, this client would pay $1,000 per year for $90,000. She was a healthy 29 year old, non smoker. If she had applied for real life insurance, say with Wawanesa or SSQ, for $1,000 per year she could have been approved for $450,000 of Term 80 Life coverage. This means she would have had $450,000 of life coverage until the age of 80, instead of only 7 years at $90,000. Put another way, this person was being ripped off. I’m not entirely sure how it’s legal, but I do know that it gives the Life insurance industry an even worse name.

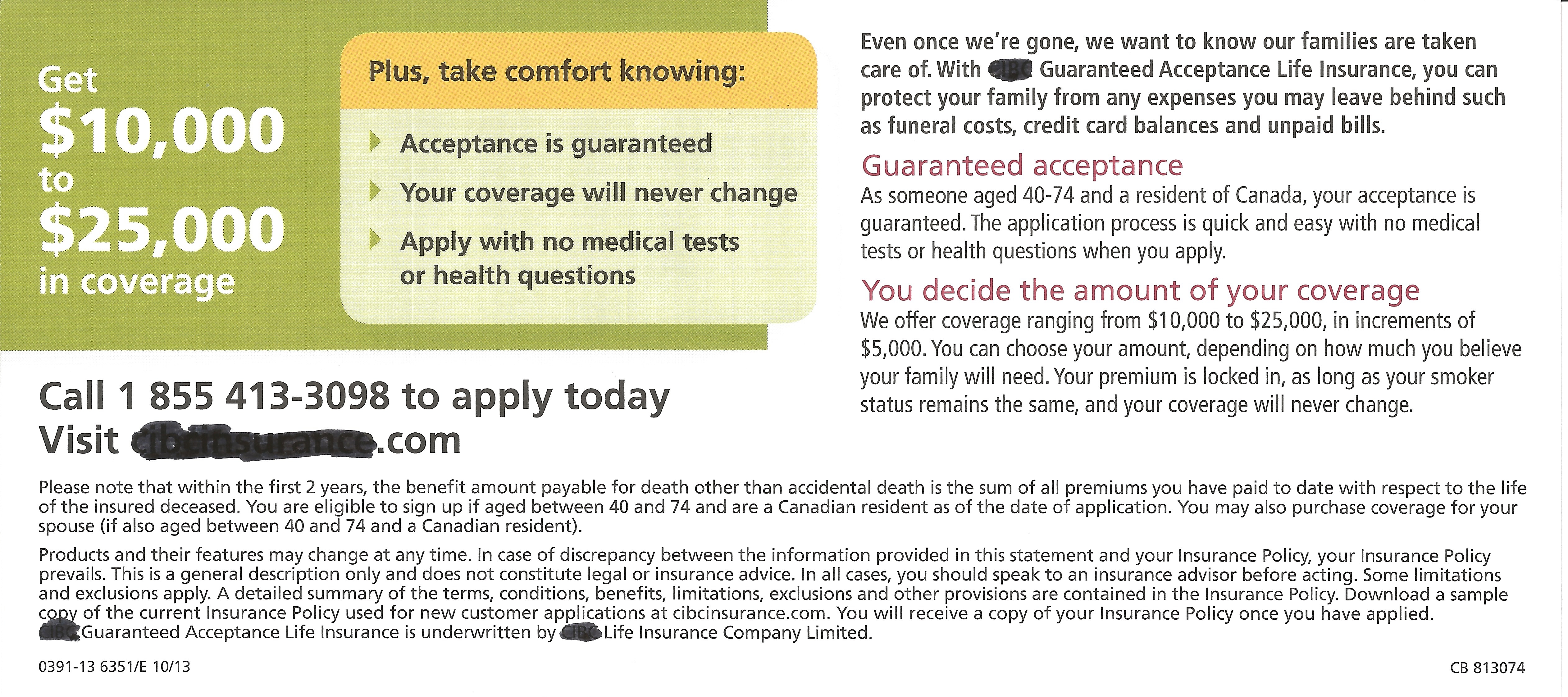

This all brings me to something I received in the mail today from my bank. It’s the document in the picture below. I’ve blackened out the name of the bank. This bank is offering $10,000 to $25,000 of “Life insurance”. Apparently acceptance is guaranteed, the coverage will never change and there is no medical or health questions. I called the number and was quoted $67.50 for $25,000 of coverage. I told them I was 40 and a non smoker.

Again, to put this in perspective, if a 40 year old male client approached a licensed broker like myself and had a budget of $67.50 per month to spend on real life insurance, I could get him $300,000 for 30 years of coverage. Would he have to take a medical? Yes. Does the bank make you take a medical? No.

But here’s the kicker. Read the small print on the document above. It reads; “Please note that within the first 2 years , the benefit amount payable for death other than accidental death is the sum of all premiums you have paid to date with respect to the life of the insured deceased.” So, if I had taken this coverage, I would have paid $67.50 per month. Say in the eighth month I have a heart attack and pass away while watching TV. Would my beneficiary receive the $25,000 that I thought I was getting? Nope, they would get $540 ($67.50 x 8 months).

If I had taken the medical and got real life insurance my beneficiary would have received $300,000. The medical is a blood and urine test and 20 minutes of questions. Maybe an hour invested to either receive $300,000 or $540.

The banks offering this type of “coverage” should be ashamed. It’s junk and people who have purchased mortgage insurance, loan insurance or “life” insurance through a bank need to look at their policies and get a licensed life insurance broker to look at it for them. There are better products at better premiums available.

Call ADI Benefits today for a complimentary quote for Life, Critical Illness, Disability, Long Term Care and Employee Health Benefits. 1-855-735-3616 or email at: info@adibenefits.ca